Peak negativity often signals the best buying opportunity

While the mixed inflation picture and August’s surprisingly strong wage growth kept a lid on UK stock prices, that cautious mood was already more than reflected in valuations up and down the market-cap scale. Swathes of the market are still dismissing UK plc, however we think the malaise is now excessive. The market is not positioned for positivity and risks missing out on a number of near-term catalysts we find compelling.

Here are three key points currently underpinning our approach to UK companies:

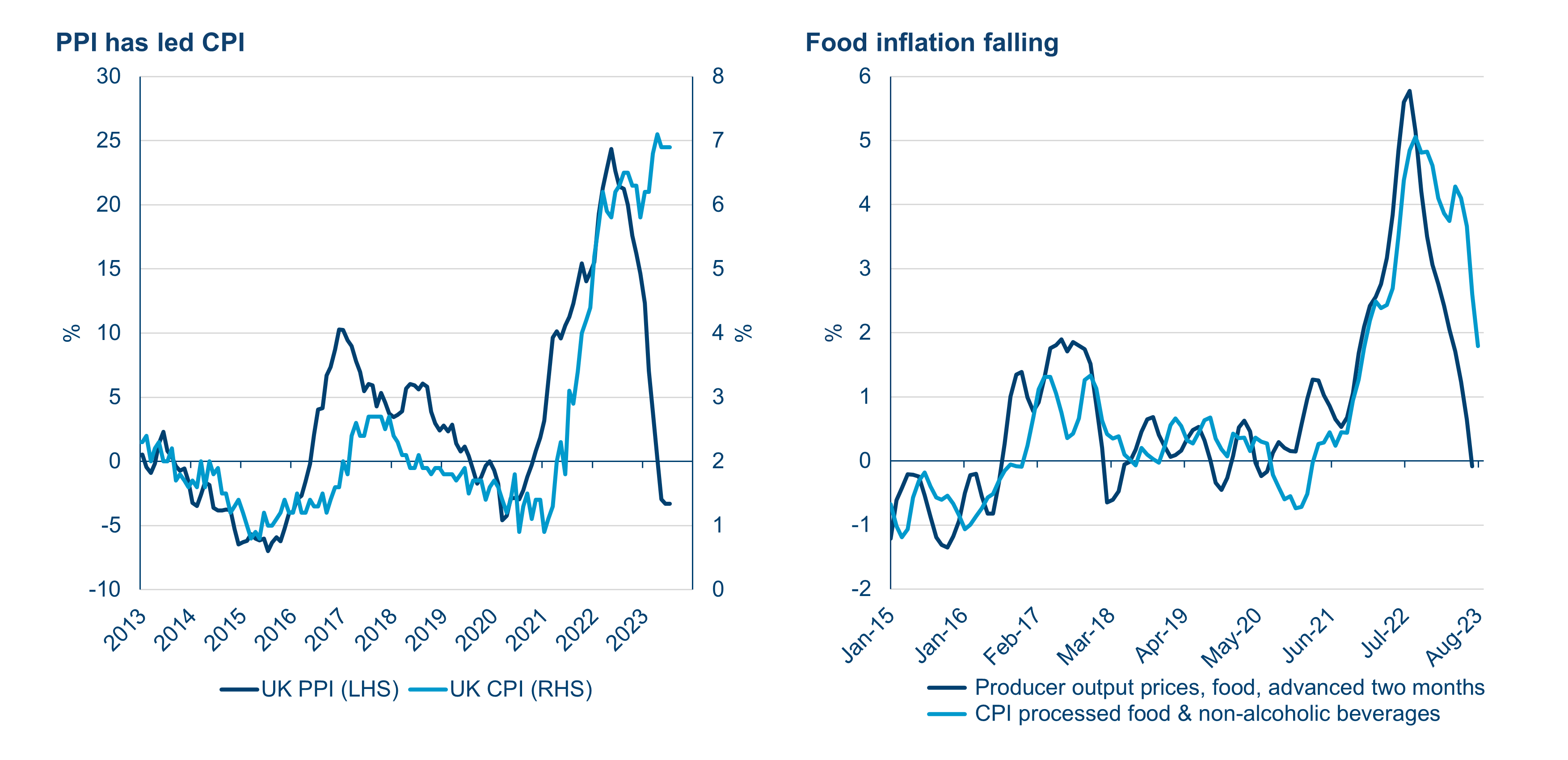

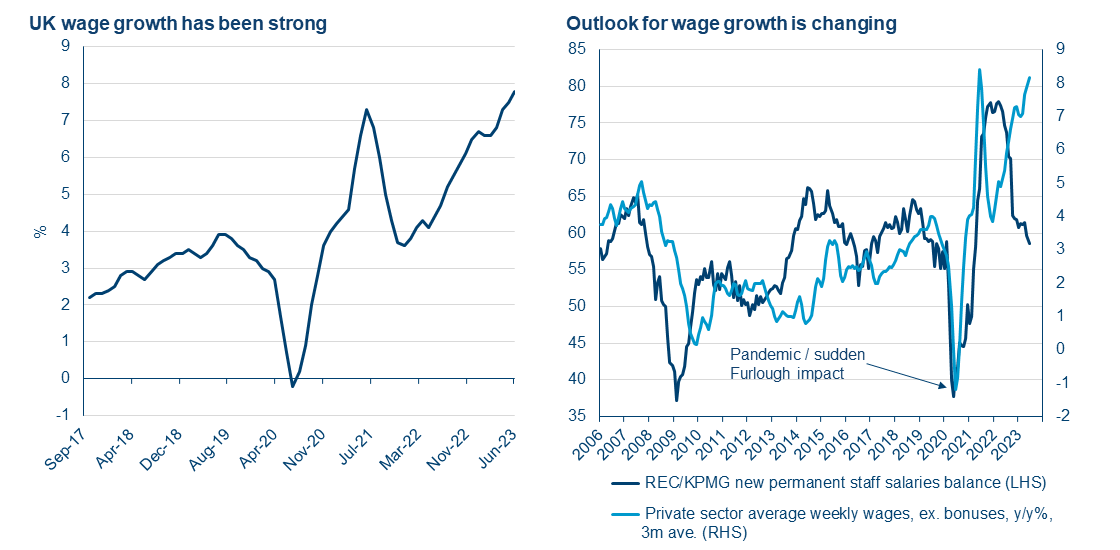

Source: Polar Capital and Bloomberg. 1. as at 31 July 2023. 2. as at 1 August 2023. Source: 1. Office for National Statistics, 30 June 2023. 2. Pantheon Macro, as at 1 June 2023. With the FTSE 250 underperforming its large-cap peers by nearly 30%1 since September 2021’s high point for mid-caps and currently trading at a c40% discount to the MSCI World Index on a P/E basis, we think the mid-tier index has been disproportionately punished. The UK’s interest rate trajectory has been a factor that has dwarfed virtually all other drivers but, even with a 25bps September rise now firmly expected, another 500bps hiking path over the next two years (in line with the rise over the past two) looks extremely unlikely. Any outsized drop in inflation beyond market consensus should lead to falling interest rate expectations and positive SMID-cap performance. As a positive indicator, UK producer price inflation (PPI) collapsed from 7.0% in March to 0.2% in May, -3.0% in June and -3.3% in July. Over the longer term, total inflation including goods and services tends to follow PPI as the latter measures price changes prior to reaching consumers. This is what we saw in the data for June and July which suggests this link is not broken. Most recently, UK wages have been growing at nearly 8%. The market has interpreted this as a sign the UK is experiencing structurally higher inflation due to a very tight labour market. If we look at the outlook for wage growth though, that is far from a foregone conclusion as shown in the chart below, right.

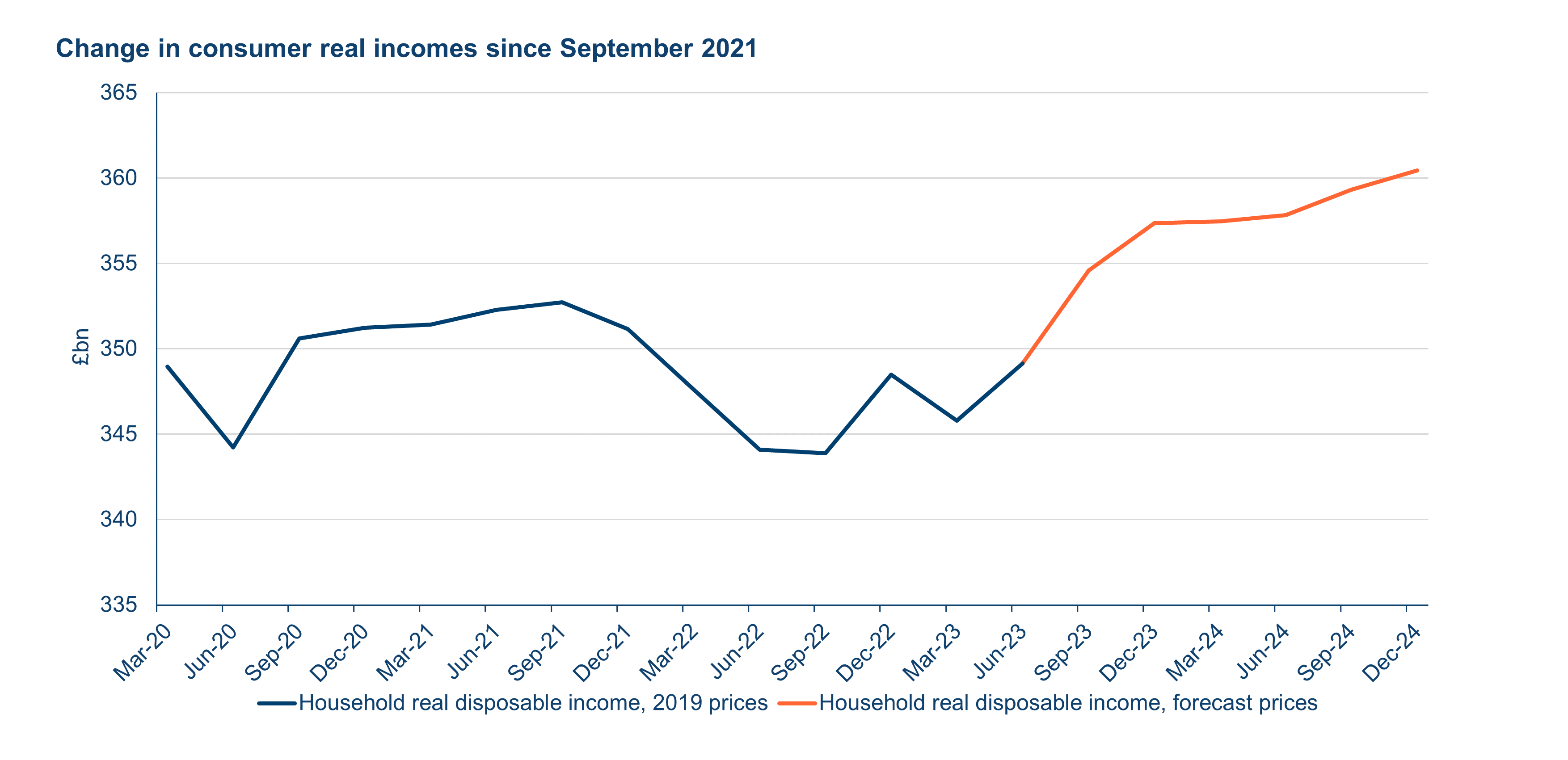

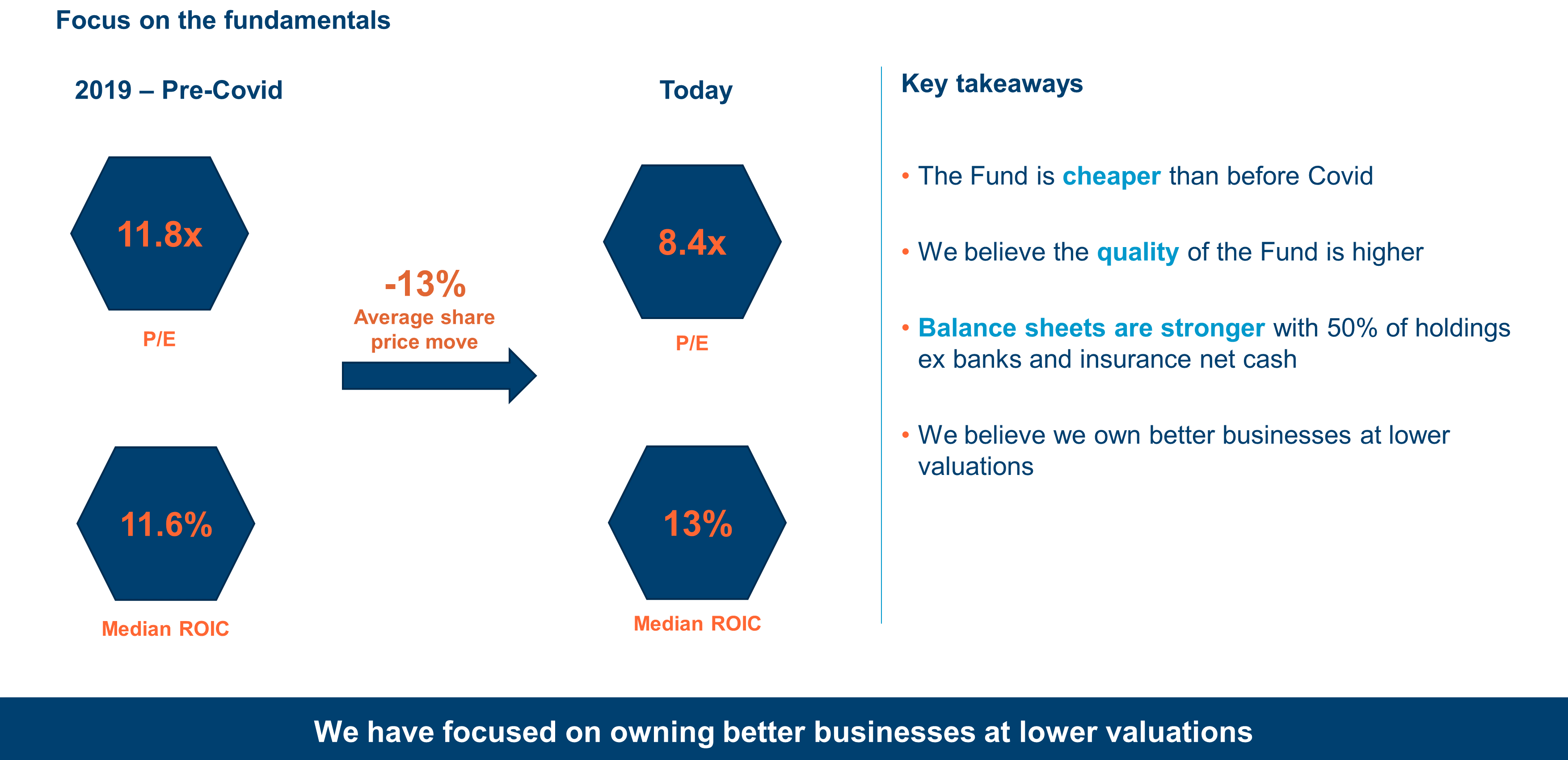

At the coalface, companies are corroborating this normalisation, having spoken to us about what they see as a much more reasonable hiring environment. There are two key drivers here; net migration to the UK has now rebounded and those who left the workforce after Covid have started to come back, prompting a rise in labour market participation. We are keen to see signs of this lag coming through. 1 Polar Capital and Bloomberg, as at 6 July 2023. Source: Pantheon Macro, as at 1 September. Household disposable incomes have suffered heavily due to the pick-up in inflation but the outlook appears considerably better from here, as shown in the chart. While increased mortgage rates will eventually affect more borrowers as home repayments rise, higher rates on savings are feeding through quicker than those on mortgages, which tend to be repriced more slowly. As around 33% of UK homes were owned outright as of 20212, according to the most recent data, savings rates initially rising faster than mortgage debts will give savers a short-term boost overall. The result is household finances will feel healthier initially and, even with higher mortgage costs eventually flipping that narrative around in 1Q24, it will coincide with expectations of rising disposable incomes next year. Moreover, after bottoming out at -49 in September 2022, GfK’s UK Consumer Confidence monitor has made its way back to -30, having reached -24 in June 2023. Inflation is still the barrier to positive readings but it is clear consumers are feeling less pessimistic, even in the face of cost-of-living struggles. 2 Housing in England and Wales - Office for National Statistics (ons.gov.uk) Source: Polar Capital UK Value Opportunities Team & Bloomberg, July 2023. Past performance is not indicative or a guarantee of future returns. The MSCI United Kingdom Index now trades at a discount of about 36% to the MSCI World Index based on forward earnings3, demonstrating the extent to which the market is snubbing the FTSE. However, while negative sentiment is undoubtedly weighing on the perception of UK companies in the short term, in the end the key driver of share price performance will be corporate profits and dividends. To that end, we have seen evidence of solid business performance in many of our portfolio companies despite the sweeping macro and index-level negativity. We now find ourselves with a Fund that we believe is higher quality than before Covid, as measured by return on invested capital (ROIC), and at a lower aggregate valuation. While the market has shown a particularly cold shoulder to the nation’s SMID-caps, the FTSE 250 and small-cap indices outperformed the FTSE 100 in July, driven by UK inflation coming in lower than consensus expectations. Should a similar set of readings create a positive catalyst into 2024, a low starting base for SMID-cap valuations will be complemented by a supportive outlook regarding underlying business performance. With earnings per share (EPS) for the FTSE 100 forecast to fall by 2.9% in the coming year, mid-cap EPS are expected to grow by 7.9%, with 11.6% anticipated for the FTSE Small Cap Index. This could suggest companies outside the topflight have the greatest opportunity to lift their valuations among all UK companies. To summarise, we believe the near term presents hurdles for the market to completely change its mind around UK SMID-cap companies, however this negativity is already reflected in valuations. Given a repeat of the reasons behind this apprehension is highly unlikely, the current environment could present an opportunity to take part in an eventual and meaningful re-rating within small and mid-caps.

Falling inflation should provide a boost for UK small and mid-caps

UK purses are set to feel fuller

Rerating potential